")

Purchasing guaranteed life insurance for seniors is the ideal option for older adults. The policy must be held for two years before benefits are paid, but it provides long-term family coverage. Top insurers expect customers to live until 90, making it an ideal time to buy. Despite its cost, guaranteed life insurance for seniors is a great way to protect loved ones from financial hardship.

Guaranteed life insurance benefits

If you’re a senior, you may be interested in guaranteed life insurance for seniors. This policy offers fixed premiums and stays in effect until a set age, usually 90 to 100 years. It costs less than term life insurance and lasts longer. The biggest advantage of guaranteed universal life insurance for seniors is that it requires no medical exam and provides lifelong coverage at a lower cost than term life insurance.

Another benefit of the best guaranteed life insurance for seniors is that it provides a death benefit in the event of the insured person’s passing. These benefits can be paid out to beneficiaries or designated causes, ensuring financial security for loved ones. Additionally, the policy remains in force as long as premiums are paid, making it a reliable financial choice for seniors concerned about the cost of long-term care. It also offers the added advantage of guaranteed cash value, providing a stable and predictable financial resource over time.

Another benefit of guaranteed term life insurance for seniors is its fewer medical requirements compared to traditional policies. With no medical exam and fixed premiums, it provides a hassle-free and predictable coverage option. It also provides greater flexibility than prepaying funeral costs, ensuring your loved ones receive financial support when needed. Although it costs more than standard term life insurance, its benefits and guaranteed approval make it a smart choice for seniors seeking long-term security.

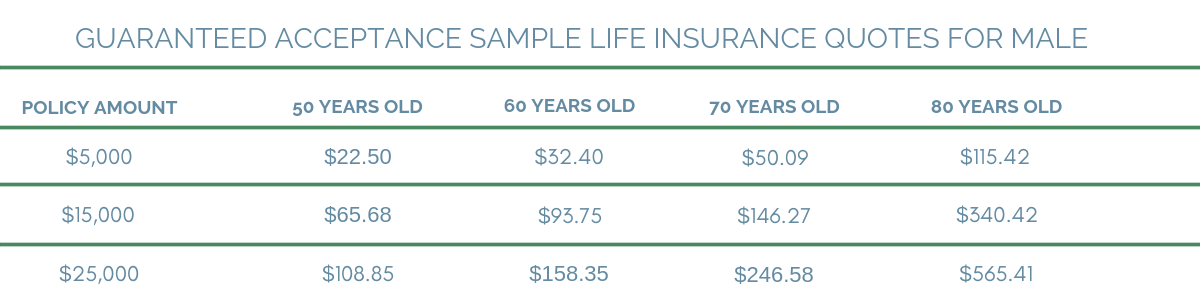

Guaranteed life insurance cost

There are many factors to consider when purchasing a guaranteed life insurance policy for seniors. These factors can include cost, coverage amount, and whether a medical exam is required. For example, the cost of a guaranteed universal life insurance policy from Mutual of Omaha is less than half of what a similar policy from another company costs. In addition, the monthly premiums are low, starting at about $8.80 a month. However, it is important to note that a guaranteed life insurance policy may only be affordable if you’re 65 years of age or older.

A policy that offers guaranteed acceptance is generally easier to obtain than other types. Applicants skip medical exams and health questions, with coverage capped at $25,000. If the insured dies within two years, beneficiaries receive a premium refund plus interest. The cost of guaranteed life insurance for seniors varies widely, based on current age and gender. A policy with a $10,000 death benefit can cost anywhere from $20 to $70 per month, depending on the provider.

As a senior, the cost of guaranteed life insurance for seniors is considerably more than a healthy individual can afford. For example, a healthy male will pay $1,122 a month to get a $250,000 death benefit, while a healthy woman can expect to pay $671 a month for a similar policy. For that amount, the coverage will last until age 90 or 100. If you are still in good health, it is a better idea to save that money for a mortgage payment.

Medical underwriting

If you’re over 80 years old, you may be wondering whether you can get guaranteed life insurance for elderly individuals without undergoing medical underwriting. While some policies offer guaranteed issue options, most insurance companies stop accepting applicants after age 80. Applicants must be mentally capable of signing a contract, so those with Alzheimer’s or cognitive impairments are ineligible. Exploring options early ensures financial peace of mind for you and your loved ones.

Insurers can offer preferential rates or surcharged premiums to those with excellent health. Some policies even exclude coverage for preexisting conditions or losses caused by specified conditions. Medical underwriting can take a couple of days or a few weeks, depending on the type of insurance and company. Insurers can still offer preferred rates to healthy people if they’re able to undergo medical tests and undergo a physical exam.

Underwriting can be done for the entire group or each individual. A small group can purchase the coverage anytime, while an employee can only join an employer’s plan during open enrollment. For a senior, a medical underwriter may review prescription medication history. While this is not required, it can be helpful to provide additional medical information or catch an oversight. Insurers may also request the information when assessing a prospective policy applicant.

The process of medical underwriting is similar to that used for life insurance. Insurers examine a person’s health history, lifestyle, and demographics. They may even contact a general practitioner or even ask the applicant to undergo a medical examination. The insurer then uses the results to determine the applicant’s rate class. They then make recommendations based on the information they have obtained. If you are under 75 years of age, medical underwriting on guaranteed life insurance for seniors is not an option for you.

Waiting period

When you apply for a life insurance policy, you must understand the waiting period. The waiting period is the period between the time you apply and when you will be covered by the policy. It is important to understand this period because it gives the insurance company time to assess you. You will not be covered if you are denied coverage. The waiting period helps the insurance company determine how much risk you pose to the company. If you pass away during this period, the insurance company will have no obligation to pay the full death benefit to your beneficiaries.

No waiting period life insurance policies are beneficial for seniors and people with chronic ailments. Seniors in good health often prefer no waiting period policies because insurance companies take on significant risk in such cases. Without a waiting period, they must pay the entire death benefit if they die soon. Because of this risk, most insurance companies have strict health requirements for those who apply for no-waiting period life insurance policies.

Age is a factor when choosing the type of life insurance policy. If you are over 70, you are more likely to have a health condition. This may make it harder to qualify for a policy or increase the cost of premiums. Some health conditions may not affect your eligibility for life insurance, but they can make your premiums higher. If your condition is more severe, you might be denied coverage. In such a case, you should consider purchasing guaranteed life insurance for seniors.

Death benefit

When a loved one dies, the days following the death can be particularly challenging. Some people depend on the income of a deceased loved one for their daily living. In such cases, a death benefit may provide the surviving family with a temporary solution. Moreover, death benefits are generally without restrictions. Beneficiaries may use the funds to meet their specific needs or deposit them in an emergency savings account. Since these funds are usually available very quickly, they can be very useful in helping to meet short-term expenses.

Although there are numerous types of life insurance, a basic plan typically offers only $3,000 in death benefits. Similarly, a graded plan may provide coverage of up to $10,000 in the first two years. It is important to note, however, that this policy has higher premiums than a traditional life insurance policy. In addition, the death benefit is typically smaller than a traditional life insurance policy’s death benefit, so a guaranteed life insurance for seniors policy may be more suitable for those with less money.

Guaranteed life insurance for seniors plans may also include a graded death benefit. In this case, the death benefit is not available immediately and may be graded over several years. After the grading period, however, the beneficiaries of a guaranteed life insurance policy will receive the full amount of the death benefit. The policyholder can designate the death benefit amount to a beneficiary or someone else. If the insured person dies during the waiting period, the death benefit is fully refundable with interest.

The eligibility requirements for a guaranteed life insurance for seniors policy vary depending on the age and health of the applicant. Aflac, for example, allows individuals over 55 to skip a medical examination. Aflac’s agents can help you figure out your eligibility for a guaranteed life insurance for seniors policy. Although guaranteed life insurance for seniors has lower rates than standard plans, it is a better option since it doesn’t require medical underwriting.