")

")

If you’re considering purchasing life insurance, it’s crucial to know the differences between term and whole life. This article will discuss Cash value, Guaranteed death benefits, Taxes, and other aspects of whole life insurance. After reading the article, you’ll have a clear idea of whether entire life insurance is the right choice for you. And what exactly is whole life insurance? What are some of the advantages and disadvantages of this type of insurance?

Cash value of whole life insurance calculator

Unlike a regular savings account, the cash value in a whole life insurance plan is a liquid asset that you can use when needed. You can access this money by taking a policy loan, making a withdrawal, or even using it to invest elsewhere. Apart from this, it acts as a valuable estate planning tool, which makes it easier to pass on money on the death of the policyholder. Unlike rigorous assets like property or stock, the cash value of your policy will not lose the value over time – it remains stable and reliable.

If you choose to borrow from the cash value of your policy, the process is easy. With interest sensitive whole life insurance, you can borrow up to the available cash value, including any interest you’ve earned. This kind of loan doesn’t count as taxable income, but it’s important to watch how much you’ve borrowed compared to your policy’s cash value. If you don’t pay the interest, it will keep adding up. Over time, if you don’t make any payments, your policy could lapse. In some cases, you may also owe income tax on the unpaid loan.

When you are thinking about how to use the cash value of your whole life insurance policy, it is important to consider the options available. For example, the most common use of cash value of whole life insurance policies is for policy loans. This type of loan has some unique advantages over a traditional loan. For one thing, it puts the policyholder in control. This makes it easier to use the money for other purposes. The cash value of a whole life insurance policy is more flexible than a traditional savings account or money market.

A cash value policy can grow a good amount of money over time. If you buy it while you’re still healthy, it can help you build a strong nest egg—but the cash value is only available during your lifetime. One of the key Whole life insurance benefits is the option to add a paid-up additions rider, which increases your death benefit and helps your cash value grow faster. If you’re considering a cash value policy, be sure to explore any extra features or benefits that can help you get the most out of your coverage.

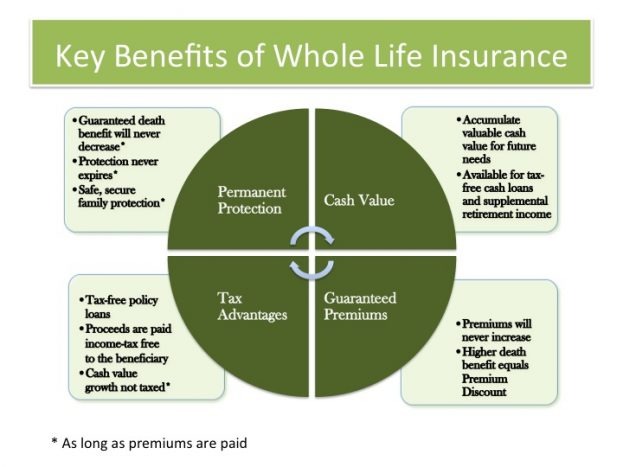

Guaranteed death benefit

A guaranteed death benefit on a whole life insurance policy provides a death benefit during the insured’s lifetime. Beneficiaries receive the death benefit tax-free, and the cash value grows on a tax-deferred basis. If you die during the year, the death benefit will be the amount of your premiums, less any interest or loan payments. You may use the additional premium payments to increase your death benefit and to pay your premiums.

The rate on a whole life insurance policy depends on your age, health, and coverage goals. This type of policy also has a guaranteed death benefit. You pay premiums in one lump sum, but you can also make monthly, quarterly, or biannual payments. The insurer invests your premiums in an account where they compound over time. When you die, your beneficiary receives the cash value. If you wish to avoid paying taxes, consider creating an irrevocable life insurance trust for your policy. This way, you can increase the number of beneficiaries and reduce your tax burden.

This type of life insurance policy can pay part of the death benefit before the insured person passes away. For example, a $1 million policy might pay $750,000 instead of the full amount. Some insurance companies automatically include this rider in all their policies. If you don’t want to pay high premiums for your whole life, you might consider a graded premium whole life insurance policy. With this option, your premiums start lower and increase gradually over time. It also allows you to lower your payments while still receiving the full death benefit if death occurs due to an accident.

Another option for increasing the cash value of your life insurance policy is to take out a loan against the cash value. This option is tax-free and allows you to withdraw money from your policy. You can also choose to divide the cash value among your beneficiaries in a manner that suits your needs. Generally, you can choose to split the loan amount equally among the beneficiaries, or assign a specific percentage to each one.

Whole life insurance cost

Whole life insurance is the most popular type of life insurance and provides up to $50,000 in coverage for life. People usually use it to cover final expenses, and it remains available until age 80. Whole-life policies do not require exams, and most companies screen medical records electronically. However, some organizations require a physical exam. For those who cannot pass the exam, whole life insurance may be the right choice. It is a great option for high-net-worth individuals and those who need to create complex end-of-life financial strategies.

The cost of whole life insurance may vary by age and sex. Generally, younger people pay lower premiums, and smokers pay higher rates. A healthy 50-year-old male can expect to pay $72 a month for a $25,000 whole-life policy. Smokers, however, will pay about $91 a month. However, younger adults are likely to qualify for cheaper rates and can lock in lower rates. Once they’ve reached their thirties, whole-life policies can be a good choice.

When looking at the cost of whole life insurance, it’s a good idea to compare whole life insurance quotes from different companies. The premium — or the amount you pay — usually goes up by about 8% to 10% each year. But the good news is that the death benefit, or the amount your family gets when you pass away, also gets higher. Your health also affects the cost. If you’re healthy, you may get lower premiums. But if you have health issues, you might have to pay more.

The cost of whole life insurance premiums can be higher than the cost of term life insurance. The higher premiums reflect the likelihood of a person’s death and are more expensive overall. Many people drop their whole life insurance policies or lower their death benefits later. The cost is appropriate for those who want to have more control over payments in their death condition. The risk of death for natural causes is also a factor in the entire life insurance premium.

Taxes

When you buy a whole life insurance policy, you’ll probably be wondering what taxes it will incur on your death benefit. This type of insurance is different from other types of insurance in that the cash value of the policy is taxable. This cash value represents the money you would receive if you died and surrendered the policy. However, there are some exceptions to this rule. You should consult a tax advisor before investing in a whole life insurance policy.

While the premiums for life insurance policies are generally tax-deductible, dividends and outstanding loan balances are not; depending on the terms of the policy, you can claim the tax benefits for the life insurance portion of the policy. The IRS has more information about life insurance taxes. When purchasing a policy for yourself or a family member, you should choose one that covers your spouse, domestic partner, or children. These policies often come with fixed dollar amounts or automatically designate the beneficiary.

Whole life insurance policies can grow in cash value above a guaranteed minimum interest rate. The gains from the cash value grow tax-deferred as long as the policy remains active. However, if you withdraw cash beyond a certain limit, it becomes taxable. You can use cash value withdrawals to cover living expenses or enjoy a long-awaited vacation. However, be aware that cashing out life insurance policies may be subject to taxes when you’ve reached a certain age.

When you die, the payouts from life insurance policies are tax-free in most cases. If you receive $1 million in death benefits from a whole life insurance policy, your beneficiaries won’t owe a cent to the federal government. However, there are some exceptions. Read up on the tax rules for each type of policy before you purchase one. Make sure you understand the rules for your state’s income taxation.

Modifications

If you are looking for an affordable final expense policy, consider a modified whole life insurance policy. These policies provide several advantages over traditional ones, such as stronger investment returns, higher initial premiums, and coverage for individuals previously declined. However, there are some things to keep in mind before making this decision. Read on to learn about the benefits and risks of these policies. For more information, contact an insurance agent.

With a modified whole life insurance policy, you pay less money upfront, but you will earn more interest over time. Because the premiums are adjusted over time, your cash value will build faster and eventually even out. However, your surrender value will be lower at first. Modifications to whole life insurance policies do offer the option of receiving life insurance dividends, but they will be much smaller than those of a traditional, fixed-premium policy.

Modified premium whole life insurance products provide a lifetime of coverage. Although these policies build smaller cash values than standard whole-life policies, you can use the dividends they generate for the same purposes. You can use the dividends to pay premiums, purchase paid-up insurance, or use them as income. However, the benefits of these policies outweigh their disadvantages.

The main drawback of modified premium whole life insurance is the waiting period required to get the death benefit. This policy is not suitable for people in the middle of the age range or who have a health condition that requires constant treatment. However, improved premium health conditions can help people get life insurance lisions. However, it is important to understand the differences between these policies to make the right decision.