")

")

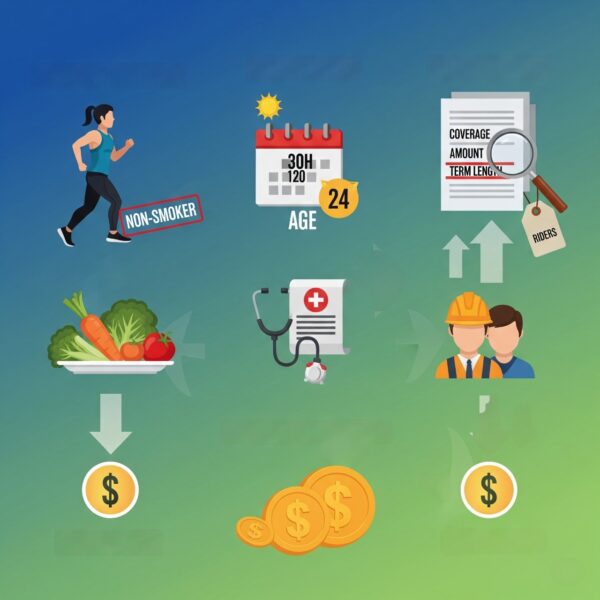

If you’re looking for the best term life insurance cost, you should know the factors that influence it. These factors include Health class, Gender, and the cash value in your Variable universal life insurance policy. Listed below are some of these factors that can affect your premiums. Keep reading for some tips that can make the process easier and save you money. The first factor to keep in mind is the length of coverage. Many term life insurance policies are for 20 years.

Factors that influence term life insurance rates

One of the first steps in reducing your life insurance premiums is to buy a term policy. A term life policy covers a specific period and requires a certain number of premiums. When the insured dies while the policy is active, the life insurance company pays predetermined amounts to the insured’s beneficiaries. A return of premium policy, on the other hand, allows the policyholder to reclaim the premiums they paid during the term.

Another essential factor to consider when determining your premiums is your coverage amount. The higher the coverage amount, the higher the premium. For example, if you want to cover yourself for a million dollars, you’ll likely pay higher premiums than someone with a policy for a few thousand dollars. Additionally, the longer the term, the higher the premiums will be. However, if you’re young and don’t expect to need insurance coverage for decades, it’s better to secure a lower premium now and have coverage later.

While age is a major factor, other elements also influence pricing. Gender is one of the most important, as insurance carriers use statistical models to estimate life expectancy for different age groups. Men are statistically more likely to die earlier, while women usually live longer. Getting a term life insurance cost estimate while you’re young can help you lock in lower rates.

Another factor that influences term life insurance premiums is the type of policy. For example, a policy with a significant benefit amount and an extended benefit period will typically cost more than a term life policy. In addition, whole life insurance policies are generally more expensive than term life policies. Lifestyle habits are also a factor in determining your premiums. Healthy lifestyle choices can reduce your cholesterol and blood pressure levels, which in turn affects your premiums.

Variable universal life insurance policy’s cash value

The owner of a variable universal life insurance policy can access it when they decide to withdraw money. The cash value grows tax-deferred, and the owner can access it by withdrawing funds or borrowing against it. However, if the cash value of the policy falls below a certain level, the owner must make additional premium payments to keep the policy active. Withdrawals made before this point may result in the account being worth less than what the owner originally invested.

Some people enjoy the flexibility of variable universal life insurance. They can also use the cash value to access a loan from a bank. In addition to paying premiums that are lower than the average, the cash value grows tax-deferred inside the policy. The policy may be a good option for investors who want a hybrid investment/insurance option. A variable universal life insurance policy can provide higher returns than other types of life insurance, give the owner more control over investments and grow tax-deferred inside the cash value.

A variable universal life insurance policy can accumulate up to six figures over decades. Unfortunately, your financial situation and retirement plan can change. Your life insurance policy may no longer make sense. You may need to use this money for unexpected expenses, and you may not be able to afford premium payments. If you can’t afford to continue paying premiums, consider investing the cash value of your policy in a mutual fund.

When choosing a variable universal life insurance policy, it’s essential to understand the risks and benefits involved. While the policy may offer a tax advantage, it also carries a significant risk of losing the principal invested. Because of these risks, it’s best to read the prospectus carefully before investing. The cash value of a variable universal life insurance policy may eventually exceed your premiums. If you dislike this risk, you may withdraw some or all of the cash value without penalty and still enjoy tax benefits.

Unlike a traditional permanent life insurance policy, a variable universal life policy allows you to invest your premiums in sub-accounts linked to the financial markets. This means that the cash value of the policy may decrease over time, potentially reducing the cash value or death benefit. A variable universal life insurance policy is tax-deferred, so the growth in cash value is not taxed. The policy allows you to transfer funds between the sub-accounts at any time.

Health class

There are a few key factors that affect the cost of health class term life insurance. Those who are overweight and have had a serious medical history will likely pay higher rates than those in a less-healthy health class. In addition, some carriers may have strict age requirements. A healthy age is 50 years old or less, and you should avoid getting a policy if you have a pre-existing medical condition.

First, you should know that health classes are based on different criteria that each insurer uses to determine the premiums you’ll pay. The factors used by these companies differ, so it’s crucial to compare rates from several different insurance companies. This way, you’ll have a better idea of which policy will cost the most. It’s also possible to choose between various health classes for different purposes. And don’t forget to compare the premiums of other providers.

Lastly, you should know that the premiums you pay depend on the health class you fall into. If you have a history of high cholesterol, high blood pressure, or heart problems, you may be in a lower health category, but you’ll still pay higher premiums. That’s because insurers use this grading system to assess the risk of any potential policyholder. It’s essential to compare rates between different health classes because it can drastically affect the cost of life insurance.

The health class used by life insurance providers to determine premiums based on your health status is based on the results of a medical exam. The names of these rating classes are different, as are the requirements for qualifying for them. Nevertheless, these guidelines can help you determine the type of coverage best suited for you. There are some fundamental differences between the health classes and the premiums for them.

Gender

You may be surprised that gender and other factors can influence the cost of your term life insurance. While you should not expect your premium to be higher, you might prefer to pay a higher premium that reflects your choices. For this reason, insurance companies often use rating variables to determine your premiums. These factors can be based on your age, gender, and other personal characteristics. However, you should remember that insurance companies cannot set premiums at such a fine-grained level.

When it comes to term life insurance, the most cost-effective strategy is to buy it when you need it—without waiting for major life events like marriage or having children. Your financial situation may require coverage at any stage. To help you understand the Term Life Insurance Cost, we gathered quotes from five leading insurers and calculated the average rate for a man in excellent health. From the same data, we also created gender-specific rate charts for women.

While gender isn’t the only or the most critical factor determining a life insurance rate, it does affect it. While your actual rate can be different from what you thought, your age and health can also affect your life insurance cost. Insurers can’t deny coverage based on your gender identity, but they can postpone your application until after gender confirmation surgery. So, how can you get the best rate? Here are some tips to help you get the best policy for the least amount of money.