")

")

To get the best term life insurance rates, you need to consider a few factors that may influence your policy’s premium. These factors include your age, gender, and health. Additionally, you should consider any medical history in your family. These factors are often overlooked in determining a good term life insurance policy rate. Read on to learn more about these factors and how they may affect your premium rate. Then, compare those factors with your specific situation and choose the most affordable policy for your needs.

Term life insurance rates by age

Age has a significant effect on the cost of term life insurance. If you are 25 years old when you purchase term life insurance, you’ll pay the lowest rate possible. However, the same policy will still cost you more than a year later when you turn 45. To understand why younger people pay less for coverage, here’s a look at term life insurance rates by age. You can also compare premium rates by gender and location to find the best rate for you.

Term life insurance rates increase every year because the policyholder’s age rises. As a rule, every birthday brings the policyholder one year closer to their life expectancy. This makes them more expensive to insure. As a result, the age of term life insurance rates increases by 5% to 8% in the 40s and 9% to 12% by the time they reach their fifties. To compensate for the age increase, insurers will average the premiums over ten, twenty, or thirty years. This way, they can make one payment over a more extended period.

The age of term life insurance rates will vary depending on your goals and age. However, it is essential to remember that age isn’t the most crucial factor when it comes to purchasing life insurance. Your reason for buying the policy is the most critical factor. For example, a 25-year-old with young children will probably need a 20-year term life insurance policy to pay for the children’s college expenses. If you’re a young adult with debt from college, however, you will most likely need a shorter policy.

Gender

For decades, auto insurers have been grappling with the issue of gender discrimination in insurance premiums. While gender does not necessarily affect insurance premiums, men and women generally pay higher rates than one another. Although gender has no legal standing to affect insurance premiums, some people are still uncomfortable with insurance premiums that are based on gender. To counter this, the U.S. government is enacting a series of laws aimed at banning gender discrimination in insurance premiums.

Although insurance companies argue that gender is an actuarially sound criterion for premiums, consumer advocacy groups have presented compelling evidence that this is not the case. For example, insurance companies often require transgender and nonbinary individuals to identify as a man or a woman on their driver’s license or birth certificate. However, the insurers cannot deny coverage based on gender identity because that could damage their image and profitability.

The projected life expectancy of a female born in 2010 is 81.4 years, while that of a male born in the same year is 75.6. This slight difference has decreased in the last 20 years and is now almost 5 years smaller than it was 20 years ago. This is reflected in the difference between male and female premiums for a seven-figure amount of life insurance coverage. The difference is more minor at younger ages, but becomes more significant as one approaches retirement age.

Health

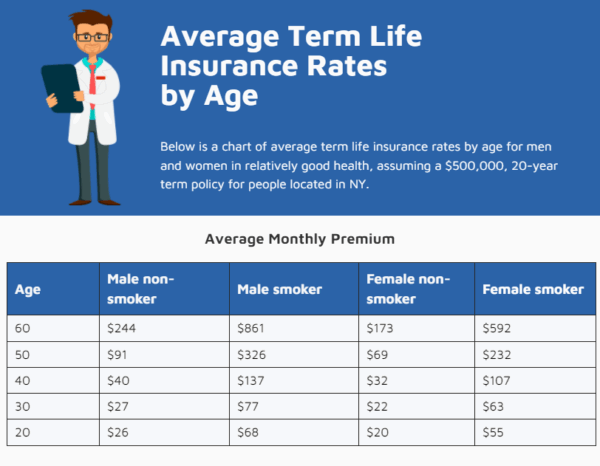

If you’re looking for health term life insurance rates, you’ve come to the right place. The following table displays health term life insurance rates for both male and female applicants. The sample monthly premium amounts are based on a composite of policies offered by Policygenius. Keep in mind that premiums will vary based on the insurer, amount of coverage and state. Rate illustrations are current as of 6/6/2022. Please note that health term life insurance premiums may be higher or lower than quoted rates.

Family medical history

When it comes to term life insurance, a family medical history has more to do with premiums than you might think. Some conditions are genetic and are passed on to future generations, which increases the risk of getting them. Others are the result of an unhealthy environment, such as being overweight or smoking. In either case, the insurance company looks for a family medical history to determine a premium. It’s also important to consider the ageing process when it comes to medical conditions.

While genetic diseases in a family history do not disqualify you from traditional coverage, they will bump you into a lower rating class, which will reduce your ability to qualify for discounted premiums. However, even with a bad family medical history, your health remains the most critical factor. Despite the health of your family, you can offset it by living a healthy lifestyle and ensuring that your family is protected.

Another factor to consider is age. If one of your parents died at age sixty-five, this could mean you are at high risk for developing breast cancer. Some companies ignore family history altogether if the insured is 65 years or older. But for a younger applicant, age is not as important. It can even affect your rate. Insurers take gender into account when determining premiums. If the family’s history is positive, it might be the key to getting a reasonable rate.

Cost

Term life insurance is much cheaper than permanent whole life. Premiums for term life insurance range from four to nine per cent higher per year. While the death benefit is generally higher, the cost per $1,000 of coverage is much lower. Typically, the best rates are reserved for young, healthy applicants. Smokers, who usually have a lower life expectancy, pay more for insurance. Smoking and health problems increase the cost of life insurance.

The cost of term life insurance can vary significantly depending on several factors, including the amount of coverage you need and the sex of the policyholder. Typical premiums can be as low as twenty dollars a month for a thirty-year-old woman, and as high as $593 for a sixty-year-old man. However, premiums rise dramatically as a person ages. In general, life insurance rates increase about nine per cent per year, so people should check their ages and health status before purchasing a policy.

The cost of term life insurance is also dependent on your health. Whether you smoke or not will determine your premiums, but a good reputation means that the company is unlikely to face financial problems. Term life insurance costs vary according to the amount of death benefit coverage you need, the length of the policy, and your age and health. If you smoke, you may find that your premiums are double or even triple what they would be otherwise. If you are a smoker, it is best to give up smoking – if only to save money and extend your life.