Before you buy an Auto Insurance Policy, you should know what you are getting. In this article, we will discuss coverage, cost, forms, and exclusions. Once you know these facts you can shop for a policy. Keep in mind that an auto policy is a legal contract, so it’s important to read it carefully before signing it. If you’re not sure how to proceed, here are some tips:

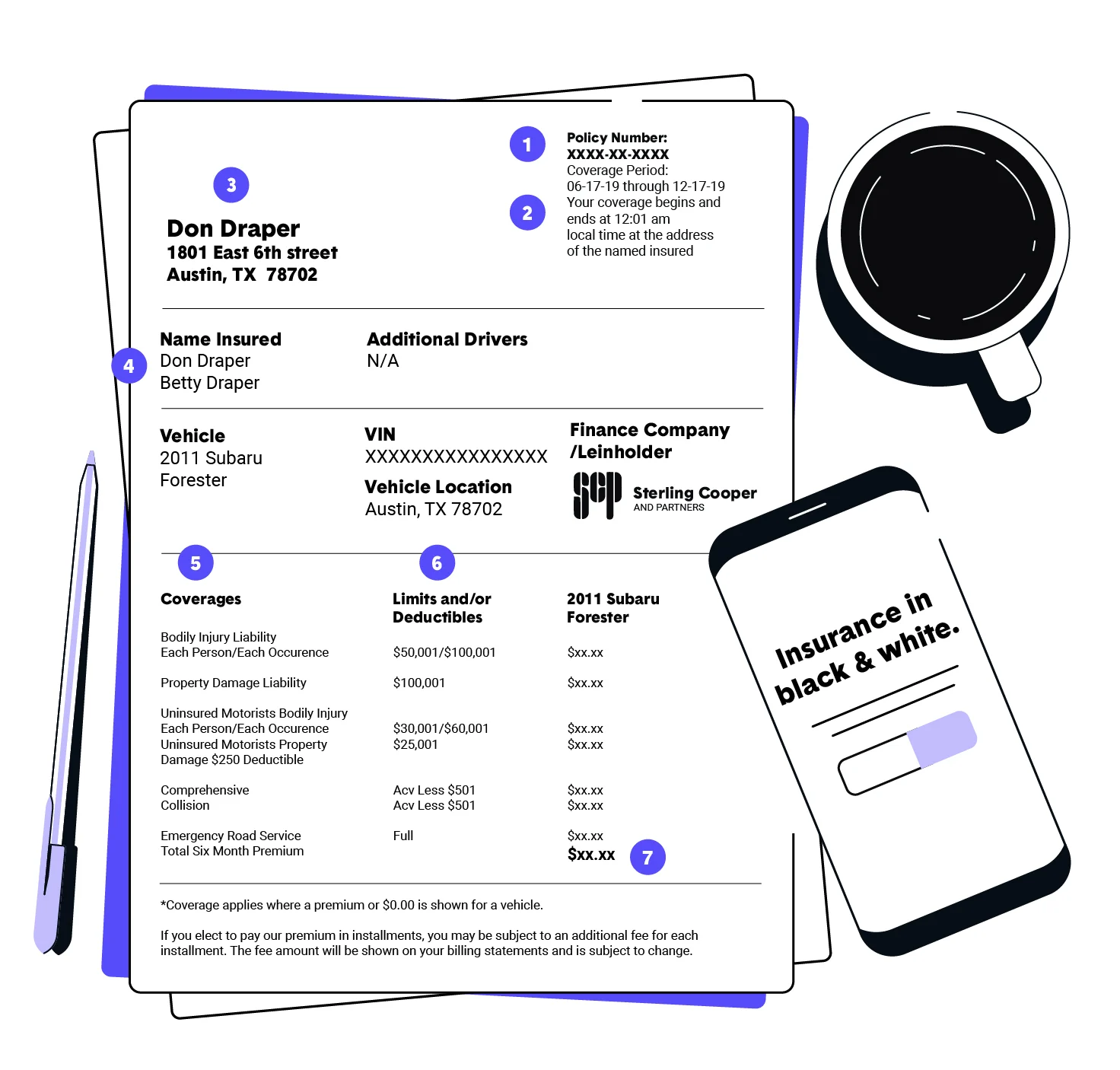

Coverage – Auto Insurance Policy

You should always be aware of the different types of coverage included in your auto policy. Your auto policy will list the covered risks and will list any exclusions or definitions. Understanding what you are covered for is important, especially if you own a high-valued vehicle. Make sure to review your policy every year to be sure it provides the coverage you need. There are also ways to lower your costs while still getting the coverage you need.

Collision and comprehensive coverage are two types of coverage you should look for. Collision coverage pays for damages caused by collisions. This type of coverage is often required by loan companies. If you buy the car outright. Collision coverage is not required. It is advisable to check the policy before making the final payment. When you buy a new vehicle. Then it can become an important feature. It can help you avoid costly repairs in the event of an accident.

Medical payment coverage is another important feature of a car insurance policy. It pays for medical expenses for policyholders and passengers. You can use it to pay for funeral expenses as well. In addition, personal injury protection coverage pays for damages you cause to other people’s property. Medical payments are usually included, but other types of property damage may also be covered. For example, damage to a lamp post or a building may be included in your liability coverage.

Cost – Auto Insurance Policy

While the average cost of an auto insurance policy varies by state, the overall average price is higher in Michigan than in any other state. In other words, you pay more for car insurance in Michigan than you do in any other state, even if you get more coverage. In addition to driving more, a sports car’s top speed also increases your insurance rate, and the same applies to an electric vehicle’s battery, which costs thousands of dollars to replace.

The age of the driver is another factor that influences the cost of coverage. Young drivers generally pay the highest rates, and their premiums increase rapidly as they approach the age of 70. Statistically, young drivers are more likely to crash than older drivers. and therefore presents a greater risk to security providers. On the other hand, middle-aged drivers generally pay the lowest premiums. That’s with an average premium of $1,379 a year for a 20-year-old driver.

Form

The auto policy form is an important document for insurance consumers. It details the terms of your auto insurance policy, its effective and termination dates, and how much coverage you’re receiving. This policy also contains the details of your agreement with your insurance company. It also lists any deductibles you must pay before your insurance company will cover the financial loss. Here’s what to look for in the form. If you have questions about your policy, don’t be afraid to contact or call your insurance agent.

The general agreement section outlines the coverage that you’ll receive from the insurance company. The definitions section explains the terms used throughout the policy. A common standardized auto policy form is the Insurance Services Office’s Personal Auto Policy Form. It’s attached to the Declarations Page of the auto policy and typically has six parts: parts A, B, and C represent coverage; parts D and E contain conditions. For a comprehensive policy, the policy will also contain an insurance definition.

A business auto policy form is very important for insurance companies. It outlines the types of vehicles insured and the extent of coverage they’re providing. These forms can also help reduce future litigation. A business auto policy form will list all the vehicles covered by the contract and specify the risks that will be covered. Generally, these forms will list auto liability, physical damage, and “broadening endorsements.”

Exclusions

You’ve probably read about the auto policy exclusions – but what exactly does it mean? Here’s a quick guide to understanding them. These are the situations that your insurance policy will not cover. For example, you’ll be unable to claim damages for an incident in which you or your family member was at fault. This exclusion is designed to prevent fraud among family members and protect you against any mishaps.

First of all, auto insurance policies will not pay out for damage to your car during an HPDE event. While you might think you’re covered, if your auto is involved in an HPDE event, your insurance company is most likely not paying out for damages incurred. So, be sure to read through your policy and contact your agent for clarification. And remember to review your policy every year, since insurers have the right to change the terms of your insurance policy.

Another important auto policy exclusion is owned but unlisted vehicles. If you’re driving a vehicle that is not listed on your insurance policy, this clause will prevent you from filing a claim. In general, the more vehicles you have, the more expensive your policy will be. Therefore, it’s important to carefully read the exclusions in your policy so you know what they mean before purchasing a new one. It’s also important to make sure your policy covers the circumstances in which the insured vehicle was involved in an accident.

Notice of cancellation

When you receive a Notice of Cancellation of your auto insurance policy, you should make sure to read it carefully. You’ll find that insurers are required to provide you with a specified period, ranging from 10 to 75 days. While most insurers are required to send you a notice, some can waive this requirement altogether. It is best to understand this period before you sign anything, as the cancellation notice is not always as helpful as you might think.

In some cases, the reason for the notice of cancellation is the fact that you have driven without insurance for several years, or have been involved in an accident. This is a violation of state law and you may be subject to penalties. While a Notice of Cancellation does not make the policy void, it extends the benefits of the notification to other parts of the policy. In some states, letting your insurance lapse will void your registration, which can have various consequences. Therefore, it is best to get this notice in a timely fashion.

A policyholder must give written notice of cancellation to the insurer if they are not satisfied with the coverage or if the policy is not being renewed. A Policyholder may send this notice by hand or first-class mail. A Registrar of Motor Vehicles must also be notified in writing of the cancellation. The policy cancellation will take effect 10 days after the written notice has been sent. However, a policyholder who receives the notice within this period may get a refund of the premiums they have paid.

Excess payment

The first thing to understand about excess coverage is that it only pays if other insurance policies don’t cover it. This type of coverage will not pay out for uninsured motorists’ insurance. Instead, it will pay out the deductible of the other coverage and any excess payments made to the other party. A medical payments policy is an insurance policy that covers a portion of medical expenses. However, a medical payments policy pays only if you have already exhausted your deductible.